Starting in March 2026, Jubilee 2000 has a new lender, not featured on comparison sites, that offers bad-credit debt-consolidation loans to UK homeowners. Here are the key features

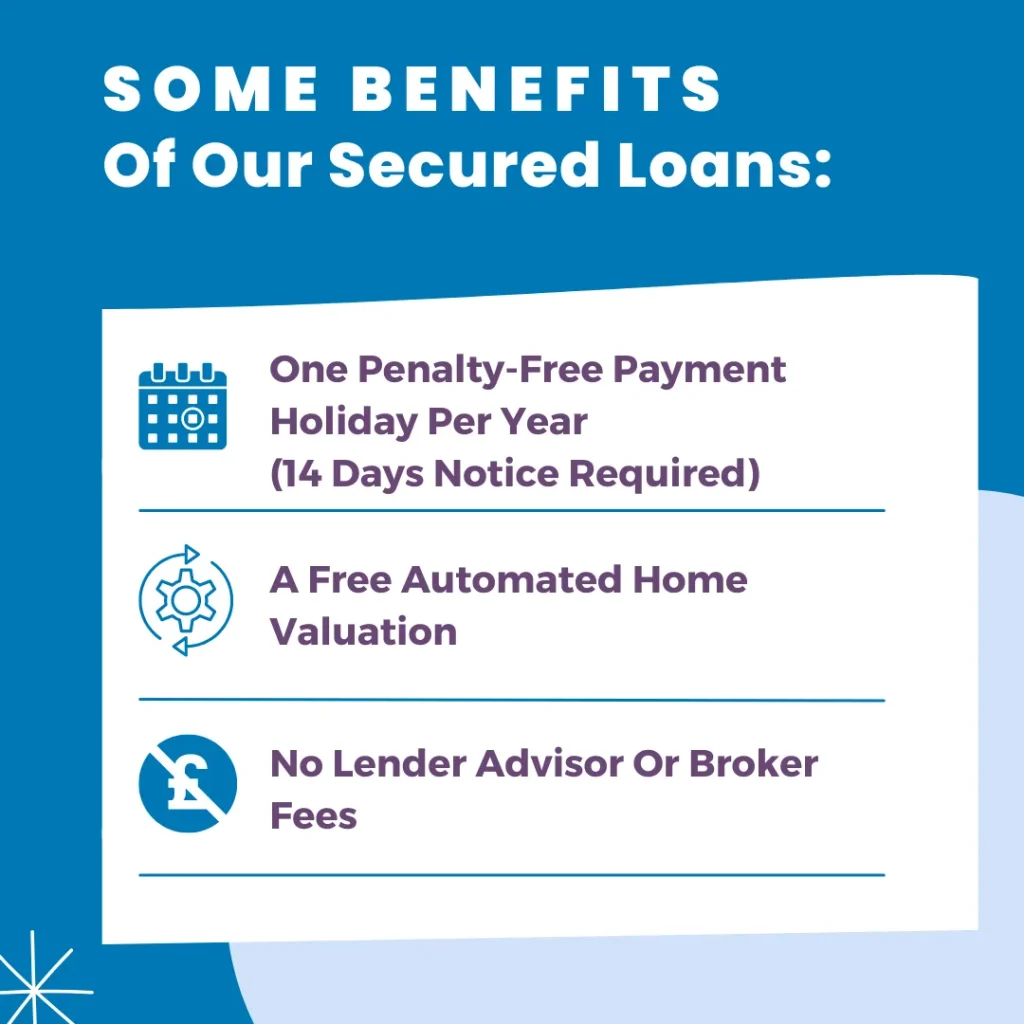

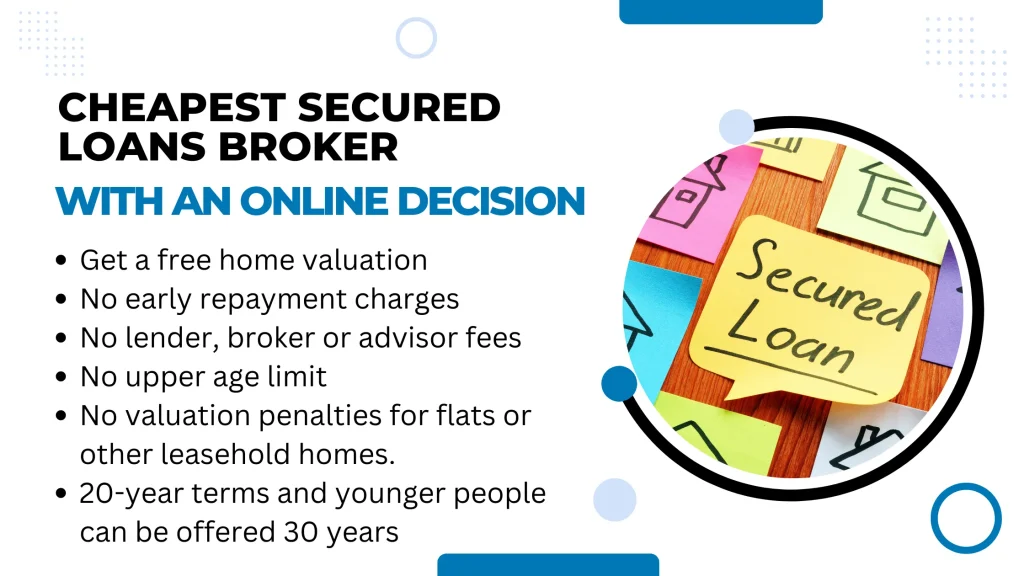

- Direct lender with no lender fees

- Instant decision based on soft credit search in the full application

- Free no obligation home valuation

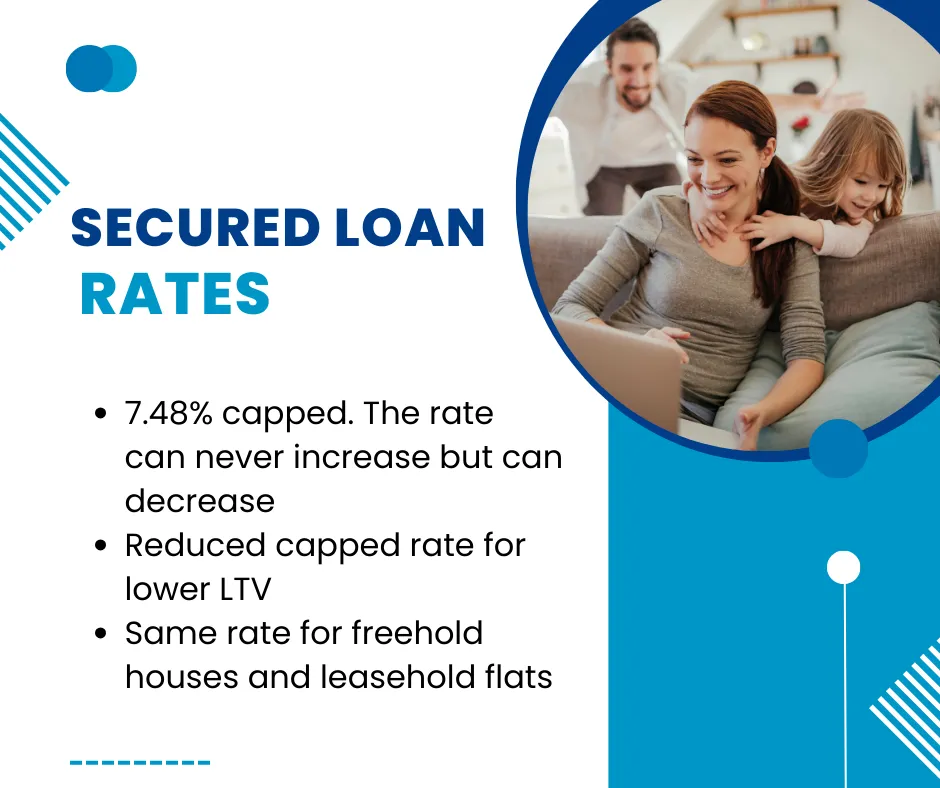

- 7.48% capped rate

- Up to 90% loan-to-value

- 2nd or 3rd charge on your home

- For existing mortgage payers only

- No broker, advisor or completion fees

- A flexible term enables up to one payment holiday per year

Please complete the form below for a decision in principle:

"*" indicates required fields

How to Get a Debt Consolidation Loan with Bad Credit from Jubilee 2000

Debt consolidation loans are an effective way to manage multiple debts by combining them into a single loan, often with a lower interest rate. However, securing a debt consolidation loan can be challenging, especially if you have a poor credit score.

Understanding the process and the factors involved can help you navigate this financial solution more effectively.

Understanding Debt Consolidation Loans

A debt consolidation loan allows you to combine several debts into one, simplifying your finances and potentially lowering your overall interest rate.

This type of loan can be particularly beneficial for those struggling with high-interest credit card debt. The goal is to reduce your monthly payments and make your debt more manageable.

Types of Debt Consolidation Loans

Debt consolidation loans can be either secured or unsecured:

- Secured Loans: These loans require homeownership.

- Unsecured Loans: These loans do not require property ownership but typically carry higher interest rates due to the increased risk to the lender.

Interest Rates for Bad Credit Secured Loans

The interest rate you can secure on a debt consolidation loan largely depends on your credit score. For those with bad credit, interest rates tend to be higher. However, understanding the typical range of interest rates and the factors influencing them can help you find the best terms.

| Loan Type | Interest Rate Range | Loan Amount |

|---|---|---|

| Secured Loan | 5% – 15% | £10,000 – £100,000 |

| Unsecured Loan | 15% – 30% | £1,000 – £25,000 |

Factors Affecting Interest Rates

Credit Score

Your credit score is a significant determinant of the interest rate on a debt consolidation loan. Higher credit scores typically qualify for lower interest rates, while lower scores result in higher rates. Lenders view borrowers with bad credit as higher risk, reflected in the interest rate.

Loan Amount and Term

The amount you borrow and the loan term also affect the interest rate. Larger loan amounts and shorter terms generally have lower interest rates. However, spreading the loan over a longer term can reduce monthly payments but increase the total interest paid.

Loan-to-Value (LTV) Ratio

The LTV ratio applies primarily to secured loans. It is the loan amount compared to the home’s value. Lower LTV ratios can lead to better interest rates because they represent less risk to the lender.

| Loan Amount | Interest Rate | Loan-to-Value (LTV) Ratio |

|---|---|---|

| £10,000 – £25,000 | 5% – 10% | 50% – 75% |

| £25,001 – £50,000 | 8% – 12% | 50% – 80% |

| £50,001 – £100,000 | 10% – 15% | 50% – 90% |

Market Conditions

Interest rates are also influenced by broader market conditions, including the Bank of England’s base rate. Economic factors such as inflation, economic growth, and market demand for credit can affect lenders’ interest rates.

Applying for a 2nd Charge Debt Consolidation Loan with Bad Credit

Applying for a debt consolidation loan with bad credit requires careful planning and understanding. Here are the steps involved:

Assess Your Financial Situation

Start by assessing your financial situation. List all your debts, including interest rates, monthly payments, and remaining balances. Understanding the total amount you owe and your current financial standing is crucial.

Check Your Credit Report

Before applying, check your credit report for errors or discrepancies. Correcting these can slightly improve your credit score, which might help you secure better terms. Tools like Experian or Equifax can provide your credit report.

Research Lenders

Research different lenders to find those specialising in debt consolidation loans for bad credit. Some lenders are more accommodating to borrowers with bad credit and offer products tailored to their needs. Consider both traditional banks and online lenders.

Compare Offers

Once you have identified potential lenders, compare their offers. Pay attention to the interest rates, loan terms, fees, and the overall cost of the loan. Using a debt consolidation calculator UK can help you understand the potential savings and costs associated with different loan options.

Prepare Documentation

Gather all necessary documentation before applying. This typically includes proof of income, identification, a list of debts, and any property information if you apply for a secured loan. Being prepared can expedite the application process.

Submit Your Application

Submit your application to the chosen lender. Ensure that all information is accurate and complete. The lender will review your application, check your credit score, and assess your ability to repay the loan.

Review the Offer

If approved, carefully review the loan offer. Pay close attention to the interest rate, loan term, monthly payment, and any fees. Make sure the terms are manageable within your budget.

Accept the Loan

If the terms are acceptable, accept the loan offer. The lender will then disburse the funds, which you can use to pay off your existing debts. Ensure you follow through by paying off the debts promptly to avoid additional interest or penalties.

Customer Reviews and Lender Reputation

Before choosing a debt consolidation loan, it’s wise to review customer feedback and a lender’s reputation. This can provide insight into the lender’s reliability, customer service, and overall loan experience. Sites like Trustpilot and Google Reviews can be useful for this purpose.

Important Review Aspects

- Customer Service: Look for reviews that discuss the lender’s customer service and support.

- Transparency: Positive reviews often mention clear and transparent terms and conditions.

- Overall Satisfaction: Consider the overall satisfaction rating of previous borrowers.

Using Homeowner Debt Consolidation Loans Effectively

Debt consolidation loans can be a powerful tool for managing debt, but they must be used wisely. Consolidating high-interest debts into a single loan with a lower interest rate can save money and simplify your financial obligations. However, it’s crucial to maintain disciplined financial habits to avoid accumulating more debt.

Creating a Repayment Plan

Before taking out a debt consolidation loan, create a detailed repayment plan. This plan should include your monthly budget to ensure you can comfortably afford the loan repayments without compromising your essential expenses.

Monitoring Your Progress

Monitor your financial progress regularly to ensure that the debt consolidation loan is helping you achieve your goals. Use tools like budgeting apps and financial planners to track your spending and repayment progress.

Example Scenarios

Consider two example scenarios to illustrate how interest rates and loan terms can vary:

Scenario 1: Secured Loan for Debt Consolidation

John has £30,000 in high-interest credit card debt. He takes out a secured debt consolidation loan using his home as collateral. The loan amount is £30,000, with an interest rate of 8% over 10 years. John’s monthly repayments are £364, and he pays a total of £13,680 in interest over the loan term.

Scenario 2: Unsecured Loan for Debt Consolidation

Mary has £10,000 in various personal loans and credit card debts. She opts for an unsecured debt consolidation loan. The loan amount is £10,000, with an interest rate of 18% over 5 years. Mary’s monthly repayments are £254, and she pays a total of £5,240 in interest over the loan term.

Easy debt consolidation loans for bad credit

When considering a debt consolidation loan, always compare offers from multiple lenders. Pay close attention to the interest rates, fees, and terms to ensure you get the best deal for your financial situation. Additionally, consider the total cost of the loan, including interest paid over the term, rather than focusing solely on monthly repayments.

By understanding the factors that influence interest rates and carefully evaluating your options, you can make a well-informed decision that supports your financial health and helps you manage your debt more effectively.

Bad Credit Debt Consolidation Loans for Homeowners

Debt consolidation loans are a valuable financial tool for homeowners looking to manage their debts more effectively, especially those with bad credit.

These loans allow borrowers to combine multiple high-interest debts into a single loan with a lower interest rate. This can simplify repayments and potentially reduce the overall cost of the debt. For homeowners with poor credit, specific options are available to help them regain control of their finances.

Understanding Bad Credit Debt Consolidation Loans

Bad credit debt consolidation loans are designed for individuals with less-than-perfect credit scores. These loans can be secured or unsecured, with secured loans typically offering lower interest rates because the borrower’s property serves as collateral. On the other hand, unsecured loans do not require home ownership but often carry higher interest rates.

Loan Amounts and Terms

The loan amount and terms can vary significantly depending on the lender and the borrower’s financial situation. For instance, a homeowner might seek a 25000 personal loan or even a 50000 pound loan to consolidate existing debts.

| Loan Amount | Interest Rate Range | Typical Term |

|---|---|---|

| £10,000 – £25,000 | 5% – 10% | 5 – 10 years |

| £25,001 – £50,000 | 8% – 12% | 5 – 15 years |

| £50,001 – £100,000 | 10% – 15% | 10 – 20 years |

Applying for a Secured Debt Consolidation Loan with Bad Credit

Applying for a debt consolidation loan with bad credit involves several steps. It is essential to understand your financial situation thoroughly and explore all available options before making a decision.

Assess Your Financial Situation

Start by evaluating your current financial status. List all your debts, including the interest rates, monthly payments, and outstanding balances. Understanding the total amount owed and your current financial standing is crucial.

Check Your Credit Report

Before applying, check your credit report for errors or discrepancies. Correcting these can slightly improve your credit score, which might help you secure better terms. Tools like Experian or Equifax can provide your credit report.

Research Lenders

Research different lenders to find those specialising in debt consolidation loans for bad credit. Some lenders are more accommodating to borrowers with bad credit and offer products tailored to their needs. Consider both traditional banks and online lenders.

Compare Offers

Once you have identified potential lenders, compare their offers. Pay attention to the interest rates, loan terms, fees, and the overall cost of the loan. Using a loan calculator consolidation can help you understand the potential savings and costs associated with different loan options.

Prepare Documentation

Gather all necessary documentation before applying. This typically includes proof of income, identification, a list of debts, and any collateral information if you apply for a secured loan. Being prepared can expedite the application process.

Submit Your Application

Submit your application to the chosen lender. Ensure that all information is accurate and complete. The lender will review your application, check your credit score, and assess your ability to repay the loan.

Review the Offer

If approved, carefully review the loan offer. Pay close attention to the interest rate, loan term, monthly payment, and any fees. Make sure the terms are manageable within your budget.

Accept the Loan

If the terms are acceptable, accept the loan offer. The lender will then disburse the funds, which you can use to pay off your existing debts. Ensure you follow through by paying off the debts promptly to avoid additional interest or penalties.

Fees Associated with Debt Consolidation Loans

When considering debt consolidation loans, it’s essential to understand the various fees that may apply. These fees can significantly increase the loan’s overall cost.

| Fee Type | Amount |

|---|---|

| Lenders Arrangement Fee | £100 – £500 |

| Valuation Fee | £150 – £300 |

| Early Repayment Charge | 1% – 5% of the loan amount |

Example Scenarios

Consider two example scenarios to illustrate how interest rates and loan terms can vary:

Scenario 1: Secured Loan for Debt Consolidation

John has £30,000 in high-interest credit card debt. He takes out a secured debt consolidation loan using his home as collateral. The loan amount is £30,000, with an interest rate of 8% over 10 years. John’s monthly repayments are £364, and he pays a total of £13,680 in interest over the loan term.

Scenario 2: Unsecured Loan for Debt Consolidation

Mary has £10,000 in various personal loans and credit card debts. She opts for an unsecured debt consolidation loan. The loan amount is £10,000, with an interest rate of 18% over 5 years. Mary’s monthly repayments are £254, and she pays a total of £5,240 in interest over the loan term.

Bad Credit Debt Consolidation Loans for Homeowners

For homeowners with bad credit, debt consolidation loans can provide a lifeline for managing and reducing debt. Options such as bad credit loans with an instant decision or secured loans for poor credit can offer immediate relief and a structured path to financial stability. Similarly, a secured loan bad-credit direct lender can provide tailored solutions for those struggling with poor credit scores.

Advantages

- Lower Interest Rates: Secured loans typically offer lower interest rates than unsecured loans, even for borrowers with bad credit.

- Single Monthly Payment: Combining multiple debts into one loan can simplify your financial management.

- Potential Credit Score Improvement: Successfully managing and repaying a debt consolidation loan can positively impact your credit score.

Using guaranteed debt consolidation loans can provide a reliable option for homeowners seeking to streamline their debt repayments.

Poor Credit Homeowner Loans for Debt Management

Poor-credit homeowner loans are designed to help individuals with less-than-perfect credit scores manage and reduce their debt. These loans are secured against the borrower’s property, offering lower interest rates and more favourable terms than unsecured loans. For example, a homeowner’s loan broker can help you find the best loan options tailored to your needs.

How to Use Homeowner Loans for Debt Management

- Assess Your Debt: Determine the total debt you need to consolidate and your current financial situation.

- Explore Loan Options: Research different lenders and compare their offers using tools like a loan calculator for debt consolidation.

- Prepare for Application: Gather necessary documentation and ensure your credit report is accurate.

- Submit Application: Apply for a loan with a lender that offers favourable terms for homeowners with poor credit.

For homeowners considering a significant loan amount, options such as a 50,000 pound loan or a 25,000 personal loan can provide the needed funds to manage and consolidate debt effectively.

Remortgaging to Pay Off Debts

Another viable option for homeowners is to remortgage their property to pay off debts. This involves replacing your existing mortgage with a new one, possibly with a higher loan amount to cover your debts. For instance, a nationwide debt consolidation mortgage can help streamline your debt into a single, manageable payment.

Benefits of Remortgaging

- Lower Interest Rates: Mortgage rates are typically lower than unsecured loan rates, even for borrowers with bad credit.

- Extended Repayment Terms: Mortgages often have longer repayment terms, which can lower monthly payments.

- Improved Cash Flow: Consolidating debt into your mortgage can free up cash flow by reducing monthly debt payments.

Considering the best bad credit mortgage lenders in the UK can provide options tailored for those with poor credit histories.

Can I get a consolidation loan with bad credit?

Yes, subject to your income and sufficient home equity, it is easy to get a homeowner loan with a poor credit score.

What credit score do you need for a debt consolidation loan?

Usually, a credit score of 400 or higher is required to qualify for a secured debt consolidation loan. However, some lenders are less bothered about your credit score and more bothered about your existing home equity and ability to pay.

Can I get a loan to pay off debt with a bad credit history?

Yes, as long as you have enough income to maintain the repayments and sufficient home equity, it should be easy to get a loan to repay old debts. This could also save you a significant amount of money each month.

Are debt consolidation loans bad for your credit?

No, often people discover they are excellent for people’s credit history.