Starting in March 2026, Jubilee 2000 has a debt consolidation loan lender offering a capped rate of 7.91%. Here are the key features:

- Loan secured on your home

- 7.91% capped rate

- 90% loan-to-value

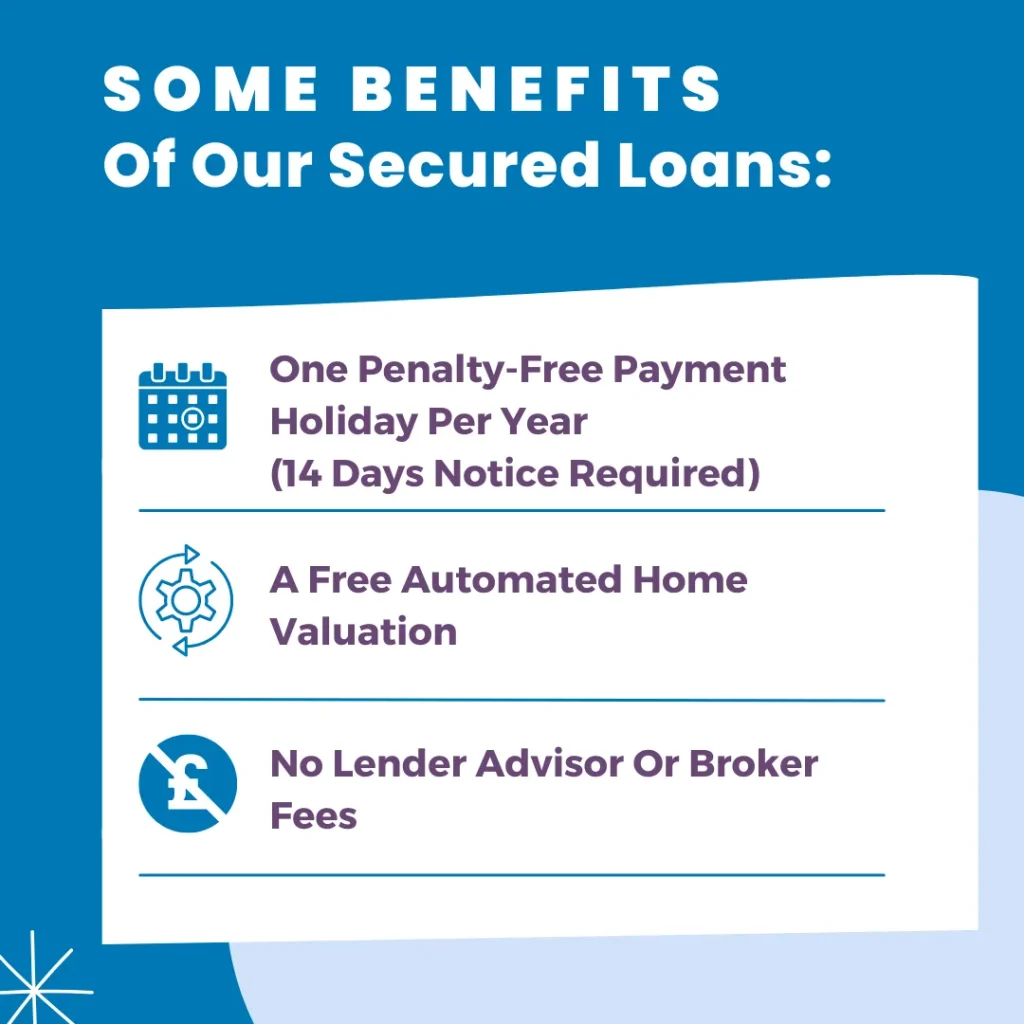

- Free valuation

- A decision in principle based on a soft credit search that has no impact on your credit file

- No lender, broker or product fees

- Direct lender

- Easy online application

- Single or joint applications

To find out more, please complete the form below:

"*" indicates required fields

Understanding Interest Rates on Debt Consolidation Loans

Debt consolidation loans are an effective tool for managing multiple debts by combining them into a single loan. The interest rate is one of the most crucial aspects to consider when opting for a debt consolidation loan. Understanding how interest rates work and what factors influence them can help you make an informed decision that benefits your financial health.

What is a Debt Consolidation Loan?

A debt consolidation loan allows you to combine several debts into one, often with a lower interest rate and more manageable monthly payments. This type of loan can simplify your finances and reduce the overall interest you pay on your debts. Debt consolidation loans can be either secured or unsecured.

Secured vs Unsecured Loans

Secured Loans: These loans require collateral, such as your home or car, which can lower the interest rate but may result in the loss of the asset if you default.

Unsecured Loans: These loans do not require collateral but usually come with higher interest rates due to the increased risk to the lender.

Interest Rates on Debt Consolidation Loans

The interest rate on a debt consolidation loan can vary widely based on several factors, including your credit score, the loan amount, and whether the loan is secured or unsecured. Generally, secured loans offer lower interest rates compared to unsecured loans.

| Loan Type | Interest Rate Range | Loan Amount |

|---|---|---|

| Secured Loan | 3% – 7% | £10,000 – £100,000 |

| Unsecured Loan | 5% – 20% | £1,000 – £25,000 |

Factors Influencing Interest Rates

Credit Score

Your credit score is a significant determinant of the interest rate on a debt consolidation loan. Lenders use your credit score to assess your creditworthiness. Higher credit scores typically qualify for lower interest rates.

Loan Amount and Term

The amount you borrow and the loan term also affect the interest rate. More significant loan amounts and shorter terms generally have lower interest rates. However, spreading the loan over a longer term can reduce monthly payments but increase the total interest paid.

Loan-to-Value (LTV) Ratio

The LTV ratio applies primarily to secured loans. It is the loan amount compared to the collateral’s value. Lower LTV ratios can lead to better interest rates because they represent less risk to the lender.

| Loan Amount | Interest Rate | Loan-to-Value (LTV) Ratio |

|---|---|---|

| £10,000 – £25,000 | 3% – 5% | 50% – 75% |

| £25,001 – £50,000 | 4% – 6% | 50% – 80% |

| £50,001 – £100,000 | 5% – 7% | 50% – 90% |

Market Conditions

Interest rates are also influenced by broader market conditions, including the Bank of England’s base rate. Economic factors such as inflation, economic growth, and market demand for credit can affect lenders’ interest rates.

Fees Associated with Debt Consolidation Loans

When evaluating debt consolidation loans, it is essential to consider the fees involved. These fees can significantly increase the loan’s overall cost.

| Fee Type | Amount |

|---|---|

| Arrangement Fee | £100 – £500 |

| Valuation Fee | £150 – £300 |

| Early Repayment Charge | 1% – 5% of the loan amount |

Common Fees

- Arrangement Fee: The lender charges an arrangement fee for setting up the loan, which can range from £100 to £500.

- Valuation Fee: For secured loans, a valuation fee may be required to determine the collateral’s value.

- Early Repayment Charge: Some lenders charge a fee if you repay the loan early. This fee can range from 1% to 5% of the remaining loan balance.

Customer Reviews and Lender Reputation

Before choosing a debt consolidation loan, it’s wise to review customer feedback and a lender’s reputation. This can provide insight into the lender’s reliability, customer service, and overall loan experience. Sites like Trustpilot and Google Reviews can be useful for this purpose.

Important Review Aspects

- Customer Service: Look for reviews that discuss the lender’s customer service and support.

- Transparency: Positive reviews often mention clear and transparent terms and conditions.

- Overall Satisfaction: Consider the overall satisfaction rating of previous borrowers.

Using Debt Consolidation Loans Effectively

Debt consolidation loans can be a powerful tool for managing debt, but they must be used wisely. Consolidating high-interest debts into a single loan with a lower interest rate can save money and simplify your financial obligations. However, it’s crucial to maintain disciplined financial habits to avoid accumulating more debt.

Creating a Repayment Plan

Before taking out a debt consolidation loan, create a detailed repayment plan. This plan should include your monthly budget, ensuring you can comfortably afford the loan repayments without compromising your essential expenses.

Monitoring Your Progress

Monitor your financial progress regularly to ensure that the debt consolidation loan is helping you achieve your goals. Use tools like budgeting apps and financial planners to track your spending and repayment progress.

Government Resources and Advice

For more information on managing debt and understanding debt consolidation loans, you can visit the Financial Conduct Authority. The FCA provides valuable resources and guidance on financial products and consumer rights.

Example Scenarios

Consider two example scenarios to illustrate how interest rates and loan terms can vary:

Scenario 1: Secured Loan for Debt Consolidation

John has £30,000 in high-interest credit card debt. He takes out a secured debt consolidation loan using his home as collateral. The loan amount is £30,000, with an interest rate of 4% over 10 years. John’s monthly repayments are £304, and he pays a total of £6,480 in interest over the loan term.

Scenario 2: Unsecured Loan for Debt Consolidation

Mary has £10,000 in various personal loans and credit card debts. She opts for an unsecured debt consolidation loan. The loan amount is £10,000, with an interest rate of 12% over 5 years. Mary’s monthly repayments are £222, and she pays a total of £3,320 in interest over the loan term.

When considering a debt consolidation loan, always compare offers from multiple lenders. Pay close attention to the interest rates, fees, and terms to ensure you get the best deal for your financial situation. Additionally, consider the total cost of the loan, including interest paid over the term, rather than focusing solely on monthly repayments.

By understanding the factors that influence interest rates and carefully evaluating your options, you can make a well-informed decision that supports your financial health and helps you manage your debt more effectively.

Understanding Secured Homeowner Loans for Debt Consolidation

Secured homeowner loans, including second mortgages, are practical tools for consolidating debts, particularly credit card debt. These loans leverage the equity in your home to secure better interest rates and more manageable repayment terms. By converting multiple high-interest debts into a single loan, borrowers can simplify their finances and save money over the long term.

How Secured Homeowner Loans Work

Secured homeowner loans involve borrowing against the equity in your property. The property secures the loan amount, providing lenders with collateral, which can lead to lower interest rates compared to unsecured loans. These loans suit substantial borrowing needs, such as consolidating multiple debts.

Loan Amounts and Terms

Loan amounts can vary widely depending on the property’s equity. For instance, if you need a 25000 loan over 5 years, you can leverage the equity in your home to secure favourable terms. Larger amounts, such as loans for 50000, are also feasible depending on the property value and the borrower’s financial situation.

| Loan Amount | Interest Rate Range | Typical Term |

|---|---|---|

| £10,000 – £25,000 | 3% – 5% | 5 – 10 years |

| £25,001 – £50,000 | 4% – 6% | 5 – 15 years |

| £50,001 – £100,000 | 5% – 7% | 10 – 25 years |

Interest Rates and Loan-to-Value Ratios

Interest rates on secured homeowner loans are influenced by several factors, including the loan-to-value (LTV) ratio. The LTV ratio is the loan amount divided by the property’s appraised value. Lower LTV ratios generally attract better interest rates because they reduce the lender’s risk.

| Loan Amount | Interest Rate | Loan-to-Value (LTV) Ratio |

|---|---|---|

| £10,000 – £25,000 | 3% – 5% | 50% – 75% |

| £25,001 – £50,000 | 4% – 6% | 50% – 80% |

| £50,001 – £100,000 | 5% – 7% | 50% – 90% |

Applying for a Secured Homeowner Loan

Applying for a secured homeowner loan involves several steps. First, determine the equity in your property. This can be done through a professional appraisal or an estimate from a local real estate agent. Next, compare offers from various lenders to find the best rates and terms. Using a debt consolidation calculator UK can help you understand the potential savings and costs of different loan options.

Steps in the Application Process

- Evaluate Equity: Determine the current market value of your property and the outstanding mortgage balance.

- Shop Around: Compare offers from different lenders, focusing on interest rates, terms, and fees. Consider using a secured loans broker for expert advice.

- Submit Application: Provide detailed information about your income, employment, and debts. The lender will conduct a credit check and evaluate your property’s value.

- Review Offer: Carefully review the loan offer, including the interest rate, repayment term, fees, and any early repayment penalties.

- Accept Offer: If satisfied with the terms, accept the loan offer and proceed with the lender’s requirements.

- Property Valuation: The lender will conduct a valuation to confirm the property’s value and available equity.

- Receive Funds: Once all checks are completed, the loan funds will be released.

For example, using a secured loan for debt consolidation can simplify your financial obligations by consolidating multiple high-interest debts into a single loan with a lower interest rate.

Secured Loans for Bad Credit

You might still be eligible for a secured homeowner loan if you have a less-than-perfect credit score. There are specific products tailored for individuals with poor credit, such as bad-credit secured loans from a direct lender and no-credit-check necessary secured loans. These loans often come with higher interest rates due to the increased risk to the lender.

Benefits of Secured Loans for Bad Credit

- Access to Funds: Secured loans provide access to funds that might not be available through unsecured loans.

- Lower Interest Rates: Even though secured loans for bad credit typically have higher rates than prime loans, they are still lower than unsecured loans for bad credit.

- Credit Improvement: Regular repayments can help improve your credit score over time.

For example, a fast secured loan can provide quick access to the funds you need, helping you manage and consolidate debt more effectively.

Secured Homeowner Loans to Repay Credit Card Debt

Secured homeowner loans can be a practical way to repay credit card debt. By consolidating high-interest credit card balances into a lower-interest secured loan, you can save money on interest and simplify your debt repayments. For example, using a credit card consolidation loans can significantly reduce your monthly payments.

Advantages

- Lower Interest Rates: Benefit from lower interest rates compared to credit cards.

- Single Monthly Payment: Combine multiple credit card payments into one manageable payment.

- Potential Credit Score Improvement: Reducing credit card balances can positively impact your credit score.

Second Mortgages for Debt Consolidation

Second mortgages, or secured homeowner loans, are another option for debt consolidation. These loans allow you to borrow against the equity in your home to pay off existing debts. For example, using a secured loan for debt consolidation can simplify your financial obligations by consolidating multiple high-interest debts into a single loan with a lower interest rate.

Benefits of Second Mortgages

- Access to Large Sums: Borrow substantial amounts to pay off significant debts.

- Lower Interest Rates: Benefit from lower interest rates compared to unsecured loans.

- Flexible Repayment Terms: Choose various repayment terms to suit your financial situation.

For instance, a second mortgage for debt consolidation can help you manage your finances more effectively by reducing multiple high-interest debts into a single, lower-interest payment.

Market Trends and Future Outlook

The UK homeowner loan market has evolved significantly, influenced by property market trends, economic conditions, and regulatory changes. As property values have risen, more homeowners have substantial equity to leverage, increasing the demand for homeowner loans.

The market has seen increased competition among lenders in recent years, resulting in more favourable terms for borrowers, such as lower interest rates and more flexible repayment options. Technological advancements have also streamlined the application process, making it more accessible and efficient.

Looking ahead, the market for homeowner loans will likely continue to grow, driven by ongoing property value appreciation and consumer demand for flexible financial products. However, economic factors such as interest rate fluctuations, inflation, and housing market stability will be crucial in shaping the future landscape.

Homeowners considering these loans must stay informed about market conditions and regulatory developments. Keeping abreast of changes in interest rates, property values, and lending practices can help borrowers make timely and informed decisions.

For more information, visit the Financial Conduct Authority.

What Is The Interest Rate On Debt Consolidation Loans, and how do debt consolidation loans work?

What is a good interest rate for debt consolidation?

A good rate is 7 and 9% for loans above £25,000 secured on your home.

Are debt consolidation loans higher interest?

No, not necessarily. Your circumstances and the LTV determine the rate you pay for the security you provide, usually your own home where you currently live.

What is the average fee for debt consolidation?

Jubilee offers debt consolidation loans with no fees, a free home valuation, and an LTV of up to 90%.

Do debt consolidation loans hurt your credit?

No, they do not hurt your credit. Many people who consolidate debts into a single monthly payment often see their credit score improve, as they no longer have loans or credit cards close to their limits.

What is the maximum you can get with unsecured debt consolidation loans?

Usually, you can get a maximum of £20,000 with an unsecured loan.